ThredUP Q1 shows consistent progress and puts new focus on Supply

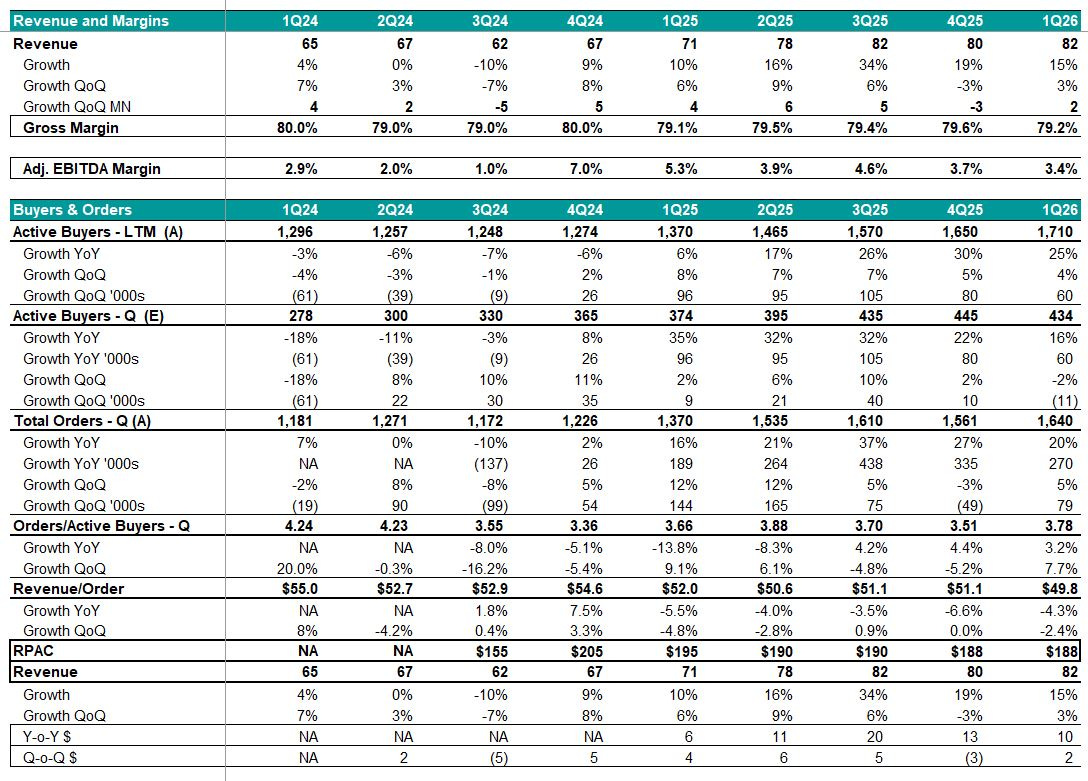

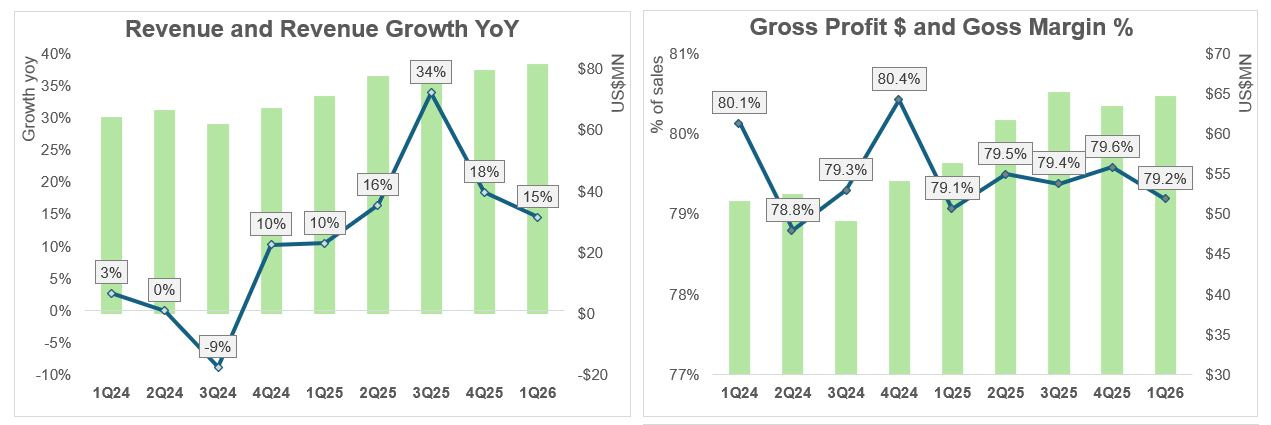

ThredUP reported a solid update for 1Q26 last week (May 4), with results coming ahead of previous guidance and rolling into an upgraded FY Outlook for Revenue, Gross Margin and Adjusted EBITDA. Active Buyers in 1Q were +25% yoy (1.71M, trailing 12 months); Orders grew in the quarter by +19% yoy to 1.6M, and Revenue were up 15% yoy, with Gross Margin remaining at a high 79.2% and Adjusted EBITDA Margin of 3.4%, 40bp above guidance.

Despite the strong results, some variables did soften during the quarter, notably Average Selling Price (~-3%) and Conversion (~-5%) moderated, which Management attributed to the Macro environment, higher fuel prices and consumer confidence coinciding with the beginning of the Iran conflict in February. Without these factors, which appear to have stabilized in Q2, Management hinted that FY guidance increase would have been more material and it has assumed no sequential improvement on these variables in the current outlook. Management also commented that frequency of purchase by existing customers continued to improve and that, in March, the company reached a new record for New Buyers growth.

Most importantly 1Q results showed consistency in execution and that the flywheel is working. 1Q was the fifth consecutive quarter of double-digit growth in Revenue and Orders, Gross Margins remained at market-leading levels of >79%, the Adjusted EBITDA Margin was positive for the 11th consecutive quarter despite higher investments in marketing and recruiting more sellers (more on this below), and the company generated Cash (1.3M) in the quarter after reaching positive FCF in FY2025.

After divesting the European business in Q3 2024, ThredUP has exceeded its guidance and raised its outlook every single quarter since (7th consecutive beats), re-building a track record of consistent and predictable performance.

Why the focus is shifting to Supply and the role of Direct Selling

The most interesting strategic update in the quarter in our view was management comments that it has started investing marketing Dollars to recruit new Sellers, not just Buyers. This is notable considering that, in the past, management often cited as a point of pride and it never spent any money to acquire sellers. Initiatives on this front included leveraging Tik-Tok shops (100,000 incremental Clean-Out kits sold in January alone), improving Sellers’ education and tools, converting more Sellers into Buyers and vice-versa, and accelerating processing in the Distribution Centers. During the call management commented that New Sellers kit requests grew by 90% year-over-year, representing 48% of total kit requests.

With 1.7M Buyers now on the platform (and growing), showing high engagement and repeat purchases, the company needs to satisfy the growing demand and higher awareness by maintaining high-quality incremental supply and faster turns to accelerate growth. This growing audience and the fact that we believe ThredUP has the fastest sell-through in the industry in the US, has also a critical impact on another important demand and supply unlock: Direct Selling.

Management was relatively cagey on the contribution of Direct Selling in the quarter, maintaining that it continues to roll-out the capability methodically, adding c. 10% incremental listings every week. During the quarter additional tools were introduced for Sellers, such as “bulk-imports” from other platforms (Poshmark, Depop etc.), reducing further the barriers-to-testing for approved users and leveraging ThredUP unrivalled tech-advantages in Digital Imagery, Pricing and Description. Management commented on further upcoming product improvements, namely in Pricing tools and in “one-click” relisting, allowing Buyers to easily relist on the platform previously purchased items, a capability unique to ThredUP. Direct Listings are still in beta and sellers continued to be capped as the number of items they can list (no luxury, maximum 30 at any given time), which speaks to management ambition to remain thoughtful as to how much, and how fast, Direct Listings should be expanded onto the market place.

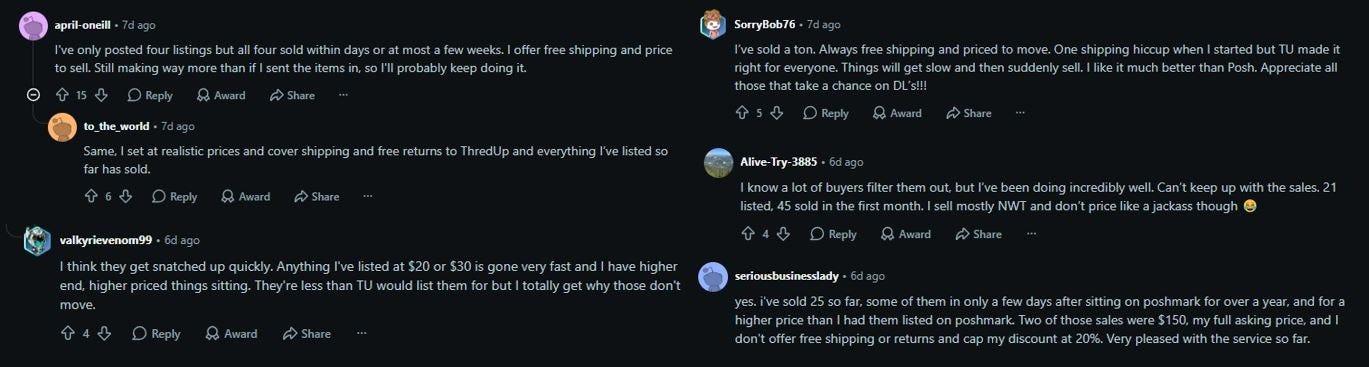

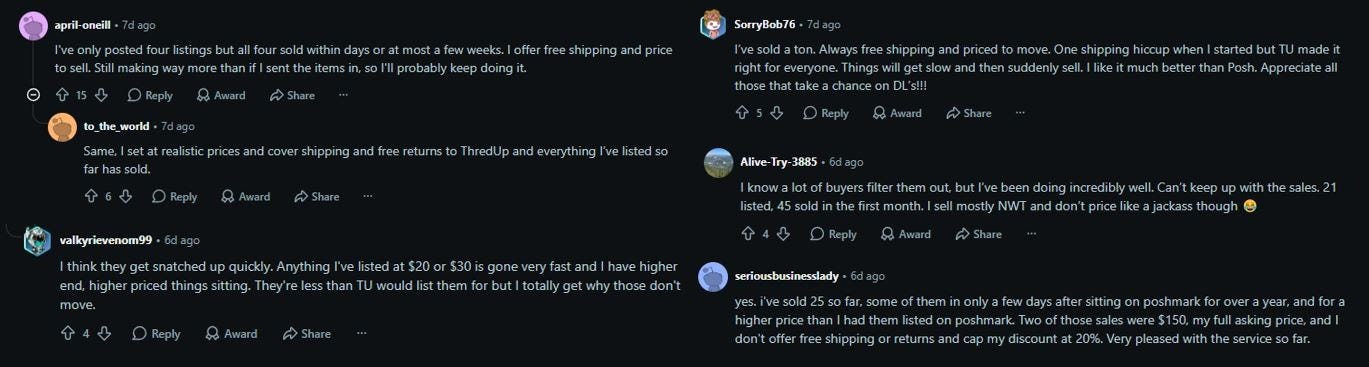

Anecdotal feedback however appears incrementally positive. When screening for customers reviews on Direct Listings on App Stores or Reddit, we noted some interesting indications:

Existing ThredUP Buyers initially complained but are now adopting the tool. When ThredUP first launched Direct Listings, we noted a number of negative comments on the different look and feel of the products compared to ThredUP core offering. These appear to have mitigated, also thanks to the continuous improvements the company has made in the presentation lay-out, and also considering that Buyers can easily decide to filter out Direct Listings.

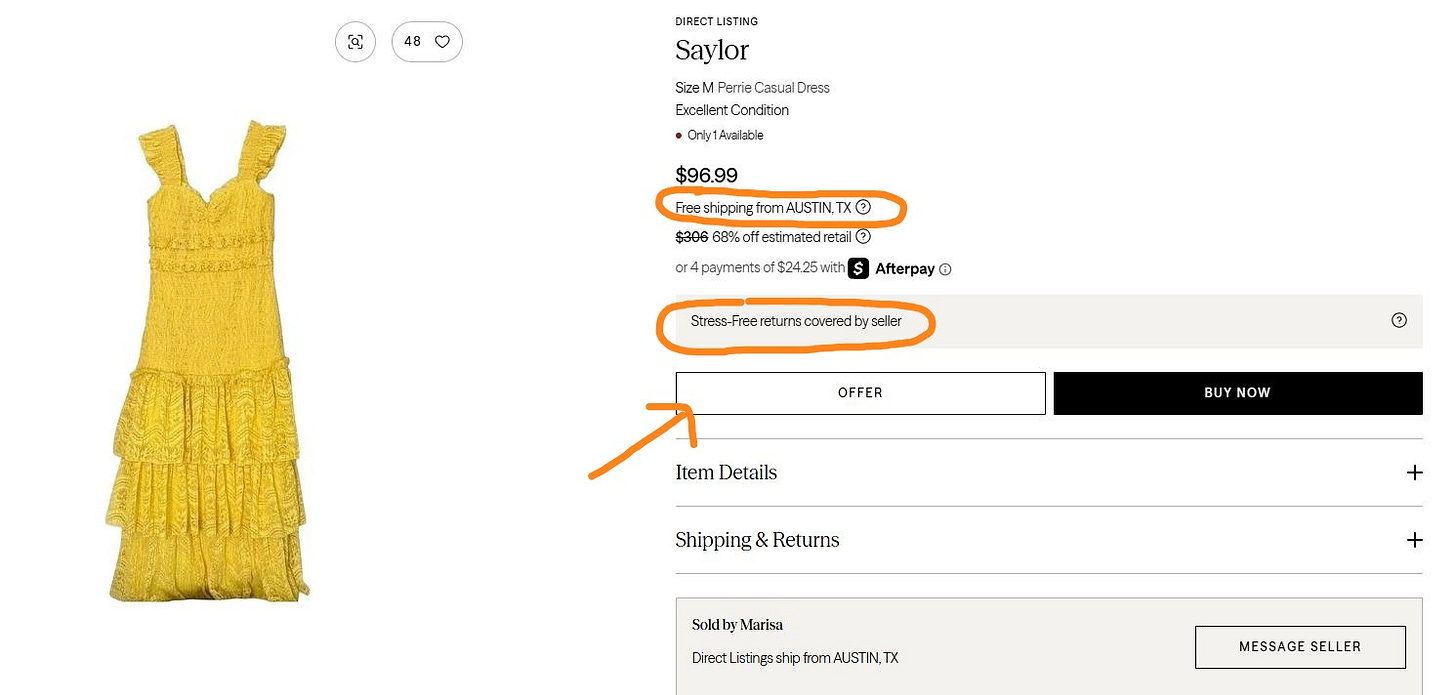

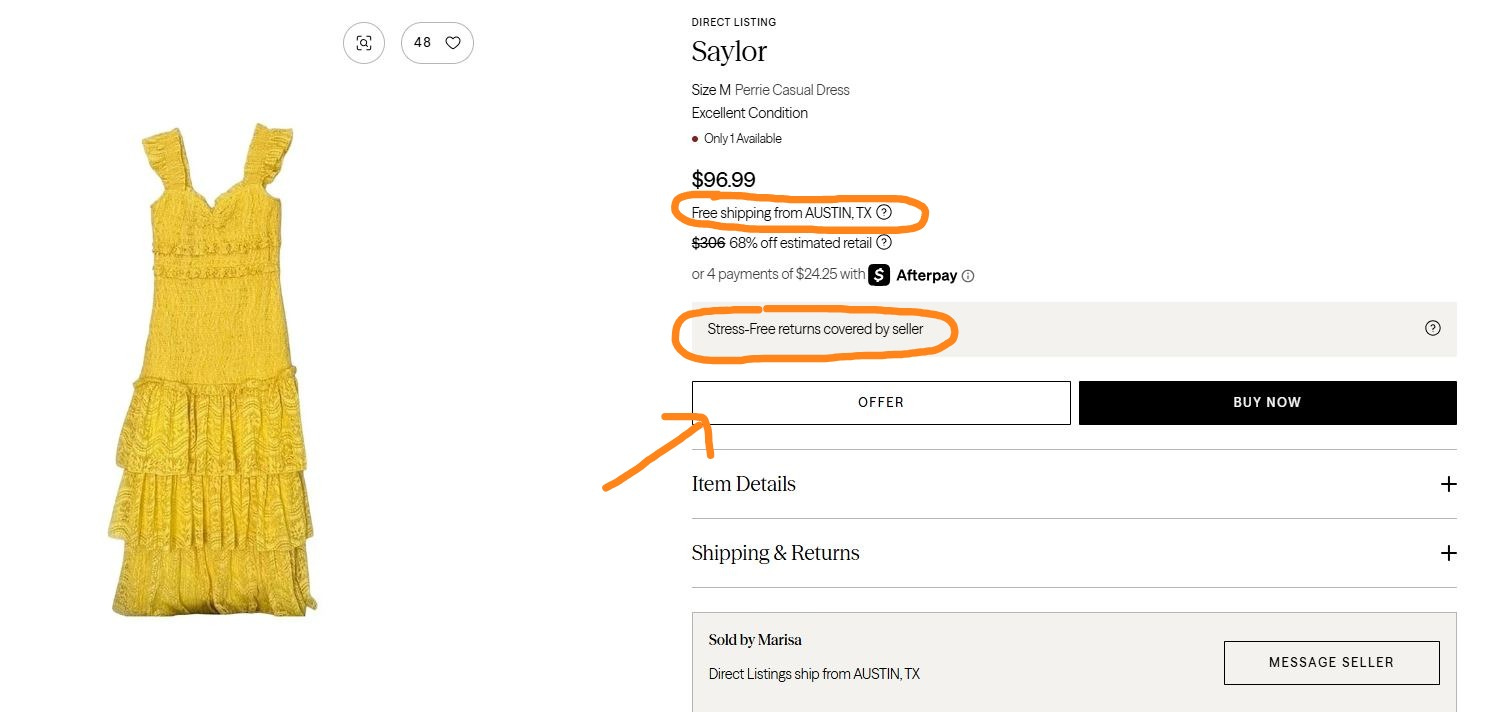

The presentation of Direct Listings is becoming more polished, blending more seamlessly with the broader offering on the Platform. Pricing is higher than traditional ThredUP listings, but it may be normalizing. Management commented in the 4Q call that Direct Listings prices were >2x higher than average (>$70), which suggested a greater mix of premium sellers than anticipated. It also generated some pushback: we noted several complaints on Reddit that some of these prices appeared unreasonably high. These comments seem to have faded recently, which may also reflect that a growing number of Sellers may now be covering Shipping and Returns fees. We also noted that ThredUP introduced a “Make an Offer” option for Direct Listings, taking a page from other peer-to-peer platforms (such as Vinted), facilitating better price-discovery.

Example of a Direct Listing where the Seller covers Free Shipping and Returns, and Buyers can offer below the listed price. Many Sellers are commenting that Direct Listings are selling more (and faster) than on other platforms. This may be the most important and relevant indicator for the success and prospects of this new growth vector for ThredUP. Sellers will ultimately migrate or co-list on the platforms that give them better sell-through and higher pay-outs. The nature of the market also means that Sellers are likely to list on more than one platform at any given time, meaning that, the greater awareness of ThredUP capabilities, the higher the chances that they will experiment with it. Ultimately Sellers will migrate to where there are more, and more engaged, Buyers. With other platforms such as Poshmark and DePop largely overwhelmed by Listings by professional sellers and a long tail of aging inventory, ThredUP approach of allowing supply to grow methodically may be setting the base for a more liquid and efficient marketplace for casual Sellers, which are the company’s focus.

Examples of comments from Reddit users on their success with selling Direct Listings on ThredUP.

ThredUP methodical and paced roll out of Direct Selling is strategically sound. What the company needs to avoid is growing too quickly and overwhelm the platform with an excessive amount of Sellers and items, with not enough buyers to meet the broader offering. If instead, as suggested by Management, supply keeps growing somewhat below demand, the platform can build a reputation with Sellers for offering, not just better tools and UI, but also better turns and sell-through. This will take time, but we believe it can unlock a meaningful driver of incremental growth, one which, importantly, requires limited to no additional infrastructure as opposed to the scaling of the consignment channel.

By the end of 2026 we expect Direct Selling to become a more visible, material and significant contributor to both revenue and supply growth, and a new strategic pillar in the Equity story. We would not be surprised if by the end of this year Direct Listings will account for 5-10% of total incremental supply on the site and a visible contributor to gross profit, before an even more material scaling in 2027.

Additional considerations on the Resale Market and competitors

In addition to ThredUP 1Q results, the past few weeks also saw several interesting updates in the Fashion Resale landscape.

The Real Real also reported 1Q figures on May 7. The “luxury-only” platform also saw healthy progress in 1Q, with sales up by 19% yoy and management raising FY targets. Notably however, different from ThredUP, the growth was mostly driven by AOV, which was up 15% yoy, while order volumes were grew more moderately. This may suggest that, while higher income consumer demand is proving resilient, the scaling of the customer base in the luxury segment may be maturing faster. Below we compare ThredUP and TheRealReal Orders, Revenue and Buyers growth. We also note that ThredUP Gross Margin in 1Q remained higher at 79.2%, compared to Real’s 74.5%.

In Europe, peer-to-peer resale platform Vinted was valued at more than U$9BN. On April 27 2026, Vinted completed a €880M secondary share transaction at an equity valuation of €8 billion, providing liquidity to existing investors and employees (no primary). In the previous secondary sale in 2024, the company was valued €5BN (60% increase). Vinted reported FY2025 revenue of €1.1BN (GMV of €10.8BN) and Adjusted EBITDA of €151MN, implying a ~7.3x EV/Revenue multiple and a ~53x EV/EBITDA.

In late February 2026, eBay agreed to acquire Depop from Etsy in a $1.2BN all-cash deal: Depop generated approximately $1 billion in GMV in 2025, or c. US$100MN in revenue, assuming a Take-Rate of ~10%. This would imply an EV/Revenue valuation of >10x. Notably, the fate of this deal may be impacted by the GameStop proposal, announced on May 3, to acquire 100% of eBay for approximately $55.5BN (~5x EV/Revenue).

These events point to the dynamism and growing maturity of the Resale sector, which will likely continue to see consolidation and corporate activity going forward. Within this landscape we continue to view ThredUP as the most undervalued and attractive investment opportunity relative to its long-term scaling potential. With a clean balance sheet, consistent double-digit top-line growth, expanding margin, and positive FCF, we believe the company remains at the cusp of fully capitalizing on the competitive advantages it has built and compounded over the past 15 years. At current prices, the stock trades at ~1.5x EV/Sales, materially below peers and recent transaction multiples.

I, Luca Cipiccia, hereby certify that this report is for informational purposes only and reflects my personal opinions as a private investor. It is not intended as financial, legal, or investment advice, nor is it an offer to buy or sell securities. All information is based on publicly available data as of May 8 2026, and I make no guarantees about its accuracy or completeness. Investing involves risks, including the potential loss of principal, and past performance is not indicative of future results. Readers should conduct their own research and consult a qualified professional before making investment decisions. I am an investor in ThredUP, but this does not imply endorsement by the company. Use this information at your own risk.